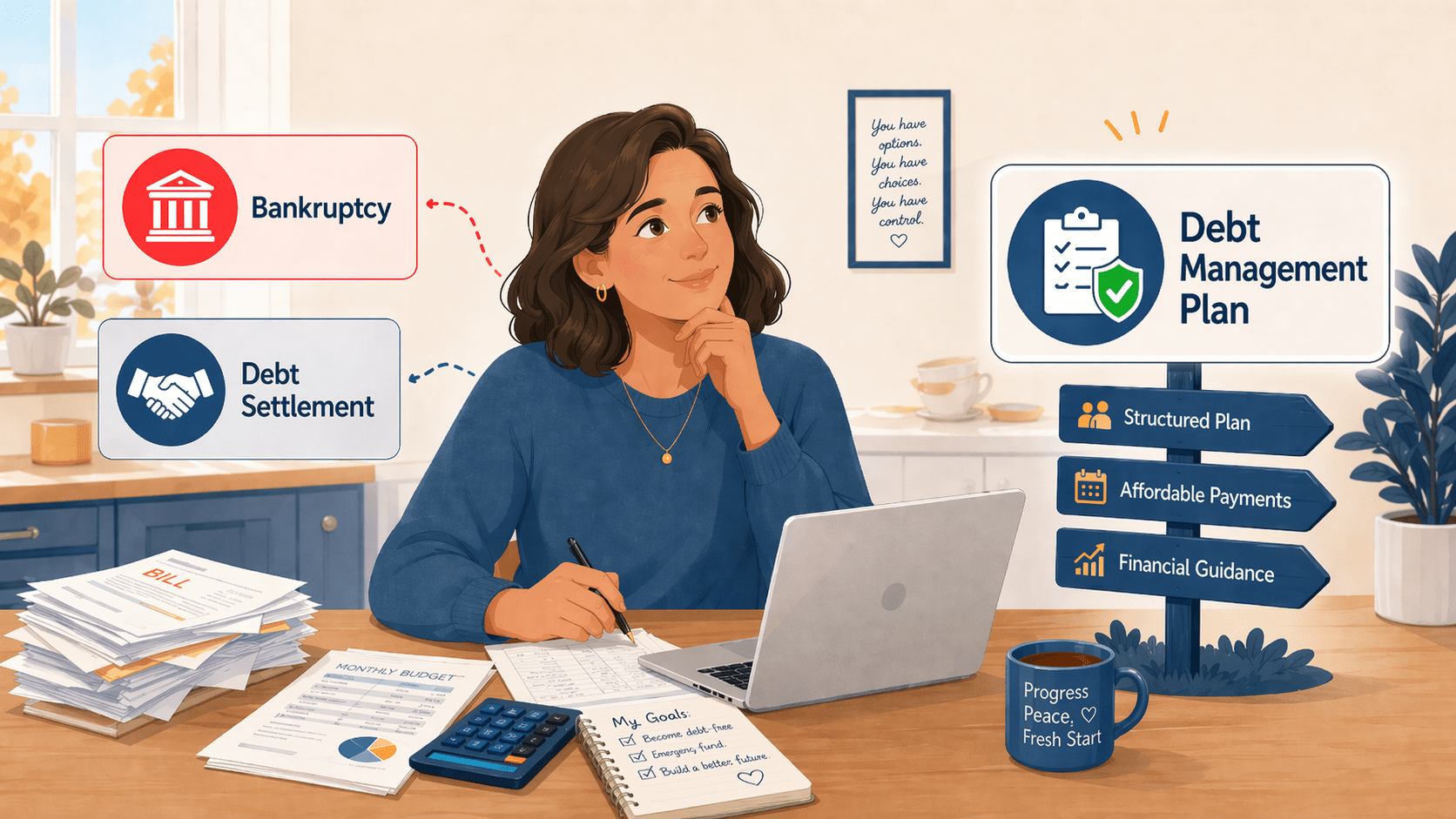

How to Choose Among Debt Relief Options: Bankruptcy, Debt Settlement, or a Debt Management Plan?

When debt starts taking over your life, the pressure to do something can feel intense. One of the hardest parts is figuring out what kind of debt relief options actually makes sense for your situation.

There are several debt relief options available, and each comes with tradeoffs. Some may reduce what you owe. Some focus on repayment. Some can have a bigger impact on your credit, your taxes, or your long-term financial flexibility.

Three of the most common debt relief options are bankruptcy, debt settlement, and a Debt Management Plan, or DMP. The right path depends on your income, your total debt, how far behind you are, and what you can realistically afford going forward.

This guide breaks down how these debt relief options work, where they differ, and what to think about before deciding.

What are the main debt relief options?

If you are looking for ways to deal with unmanageable unsecured debt, such as credit card balances, personal loans, or medical bills, you will probably come across these three debt relief options:

1. Bankruptcy

Bankruptcy is a legal process that may help people eliminate or reorganize debt when repayment is no longer realistic. It can provide meaningful relief, including the possibility of stopping collection activity, but it is also a major financial step with long-term consequences.

2. Debt settlement

Debt settlement usually involves trying to negotiate with creditors so they accept less than the full amount owed. That can sound appealing on the surface, but it often comes with risk, including ongoing delinquency, collection activity, and possible tax or legal consequences on forgiven debt.

3. Debt Management Plan (DMP)

A Debt Management Plan is typically offered through a nonprofit credit counseling agency. Instead of reducing the principal balance, a DMP focuses on repaying your debt in full, often with reduced interest rates or fee concessions from participating creditors. You make one consolidated monthly payment, and the agency distributes funds to your creditors.

Comparing debt relief options

No single solution is best for everyone. The real question is which option fits your financial reality and gives you the best chance of following through.

Here is a practical look at how these debt relief options compare.

Bankruptcy: when the debt is more than you can realistically repay

For some people in dire financial straits, bankruptcy may be the most appropriate option. If your debt load is extreme, your income is limited, or you are facing serious legal or collection pressure, bankruptcy may offer a reset that other solutions cannot.

Potential benefits of bankruptcy

Bankruptcy can stop or pause collection efforts through legal protections. Depending on the type of bankruptcy and your circumstances, it may also discharge certain unsecured debts.

For someone with no realistic path to repayment, that relief can be significant.

Potential downsides of bankruptcy

Bankruptcy is not free. There are filing costs, and many people also pay attorney fees. It also requires documentation, disclosures, and careful handling of assets, income, and debts.

It can remain on your credit reports for years, and that can affect future borrowing, housing applications, and other parts of your financial life.

Who bankruptcy may fit best

- has overwhelming debt with little ability to repay it

- is already severely behind

- is dealing with lawsuits, judgments, or aggressive collection activity

- needs legal protection, not just a lower payment

Debt settlement: lower payoff amount, higher uncertainty

Debt settlement is often marketed as a way to pay less than what you owe. In some cases, creditors may agree to settle for a reduced amount. Still, there is usually a difficult stretch before that happens.

How debt settlement generally works

Many settlement strategies depend on accounts becoming seriously delinquent before creditors are willing to negotiate. During that time, late fees and interest may continue to build, and collection calls may continue as well.

Even when settlements are reached, it can take years to resolve multiple accounts.

Risks to understand before choosing debt settlement

Debt settlement can carry real uncertainty. Credit damage is often part of the process because accounts are typically already delinquent or charged off before settlements are reached. There is also no guarantee that every creditor will agree to settle.

Some consumers may also owe taxes on forgiven amounts, depending on their circumstances, so it is smart to ask a tax professional what that could mean in your case. Some creditors may also choose to pursue legal action instead of settling.

Who debt settlement may fit best

- cannot afford full repayment

- has access to lump sums or can save for negotiated payoffs

- understands the credit and collection risks involved

- is willing to accept uncertainty in exchange for the possibility of paying less overall

Debt Management Plans: structured repayment with support

Among debt relief options, a Debt Management Plan can be a strong middle path for people who need help but still have the ability to repay what they owe over time.

How a DMP works

With a DMP, you work with a credit counseling agency to review your budget, debts, and goals. If you qualify, the agency may help set up a plan with participating creditors. You make one monthly payment to the agency, which then sends payments to your creditors.

The goal is usually full repayment over a set period, often around three to five years, with more manageable terms.

Potential benefits of a DMP

A DMP can simplify your finances by replacing multiple payments with one. It may also reduce interest rates and certain fees, which can help more of your payment go toward principal.

For people who are still trying to repay what they owe but need structure and relief, that can be a meaningful advantage.

Another benefit is guidance. A nonprofit credit counseling agency can help you understand your budget and determine whether a DMP is actually a fit, rather than pushing a one-size-fits-all answer.

Potential downsides of a DMP

A DMP is still a serious commitment. You usually need steady enough income to make the monthly payment consistently. Many plans also require enrolled credit card accounts to be closed, which can affect your credit profile over time.

And while a DMP can be more stable than some other debt relief options, it is not an instant fix. It requires discipline, follow-through, and room in your budget month after month.

Who a DMP may fit best

- has regular income

- is struggling with credit card debt

- wants to repay debt in full under more manageable terms

- would benefit from structure, payment consolidation, and nonprofit guidance

Which debt relief option hurts your credit the most?

Among common debt relief options, bankruptcy and debt settlement generally have a more severe credit impact than a Debt Management Plan.

That said, credit outcomes are not always simple. Your score may already be suffering because of high balances, missed payments, or delinquent accounts before you choose any program. A DMP can also affect your credit profile if enrolled accounts are closed or your mix of active credit changes.

A more useful question is which option helps you stop the financial damage from getting worse.

Which debt relief option is the least expensive?

That depends on how you define cost.

If you are only looking at upfront cost, bankruptcy may involve court and attorney fees, while debt settlement and DMPs may start with lower initial expenses.

But total cost is bigger than what you pay on day one. You also have to think about how much of the debt you repay, how long the process takes, whether fees are involved, whether missed payments, interest, or taxes increase the total burden, and the cost of failure if the plan falls apart.

Sometimes the option that looks cheaper at first glance ends up costing more in stress, time, or long-term damage.

How to choose among debt relief options

When comparing debt relief options, start with honesty.

- Am I able to repay my debt over time if the terms improve?

- Am I already too far behind for that to be realistic?

- Do I need legal protection?

- Can I commit to a long-term repayment plan?

- Am I looking for the lowest payment possible, or the most sustainable path out?

If you are not sure, you do not have to guess.

A reputable nonprofit credit counseling agency can review your full situation and help you understand your options without pressuring you into one path. In some cases, a Debt Management Plan may make sense. In others, it may not. The goal is to choose based on facts, not fear.

Final thoughts on debt relief options

There is no universal winner among debt relief options. Bankruptcy, debt settlement, and Debt Management Plans each solve different problems and come with different tradeoffs.

What matters most is choosing the option that matches your actual financial situation, not the one with the loudest promise.

If you are overwhelmed and do not know where to begin, a conversation with a nonprofit credit counselor can help you understand what is realistic, what is risky, and what next step may make the most sense for you.

Take Charge America is a nonprofit credit counseling agency with 40 years of experience. Start your FREE credit counseling session online here, or by calling 877-357-6309.

You can also learn more about our credit counseling services, learn more about Take Charge America, or visit our Education Center for more helpful articles.

Frequently Asked Questions

What are the main debt relief options?

The main debt relief options most consumers compare are bankruptcy, debt settlement, and Debt Management Plans. Each works differently and comes with different costs, risks, and credit implications.

Is a Debt Management Plan the same as debt settlement?

No. A Debt Management Plan generally focuses on repaying debt in full under more manageable terms, while debt settlement aims to negotiate reduced payoff amounts, often after accounts become delinquent.

Which debt relief option is best for credit?

In general, a Debt Management Plan may be less damaging to credit than bankruptcy or debt settlement, but any option can affect credit depending on your starting point and how your accounts are handled.

Can forgiven debt be taxed?

In some cases, yes. Forgiven debt may be treated as taxable income, depending on the situation. Consumers considering debt settlement should ask a tax professional how this could apply to them.

How do I know which debt relief option is right for me?

The best option depends on your debt amount, income, delinquency status, and ability to repay over time. A nonprofit credit counseling session can help you compare debt relief options based on your actual circumstances

Related Posts

Programs for Debt Relief: The 5 Types of Relief and Who They’re For

When people search for programs for debt relief, they often find a mix of options that sound similar but work…

Read More

Trump Administration Calls for 10% Credit Card Interest Rate Cap: What It Could Mean for Your Wallet.

Credit card interest rates have been incredibly high for American families. If you’ve been carrying a balance recently, you’re likely…

Read More

What Is the 50-30-20 Budget Rule? A Simple Guide to Smarter Budgeting

Many consumers like to have guidelines for budgeting and other financial planning decisions. They want to know how much to…

Read More