Programs for Debt Relief: The 5 Types of Relief and Who They’re For

When people search for programs for debt relief, they often find a mix of options that sound similar but work very differently. Some are designed to help you repay what you owe in a structured way. Others focus on settling debt for less than the full balance. Some are temporary. Some have serious long-term consequences.

The right choice depends on your income, credit, how far behind you are, and whether your debt problem is short-term or ongoing.

Here is a simple way to think about the five main programs for debt relief and who each one is actually for.

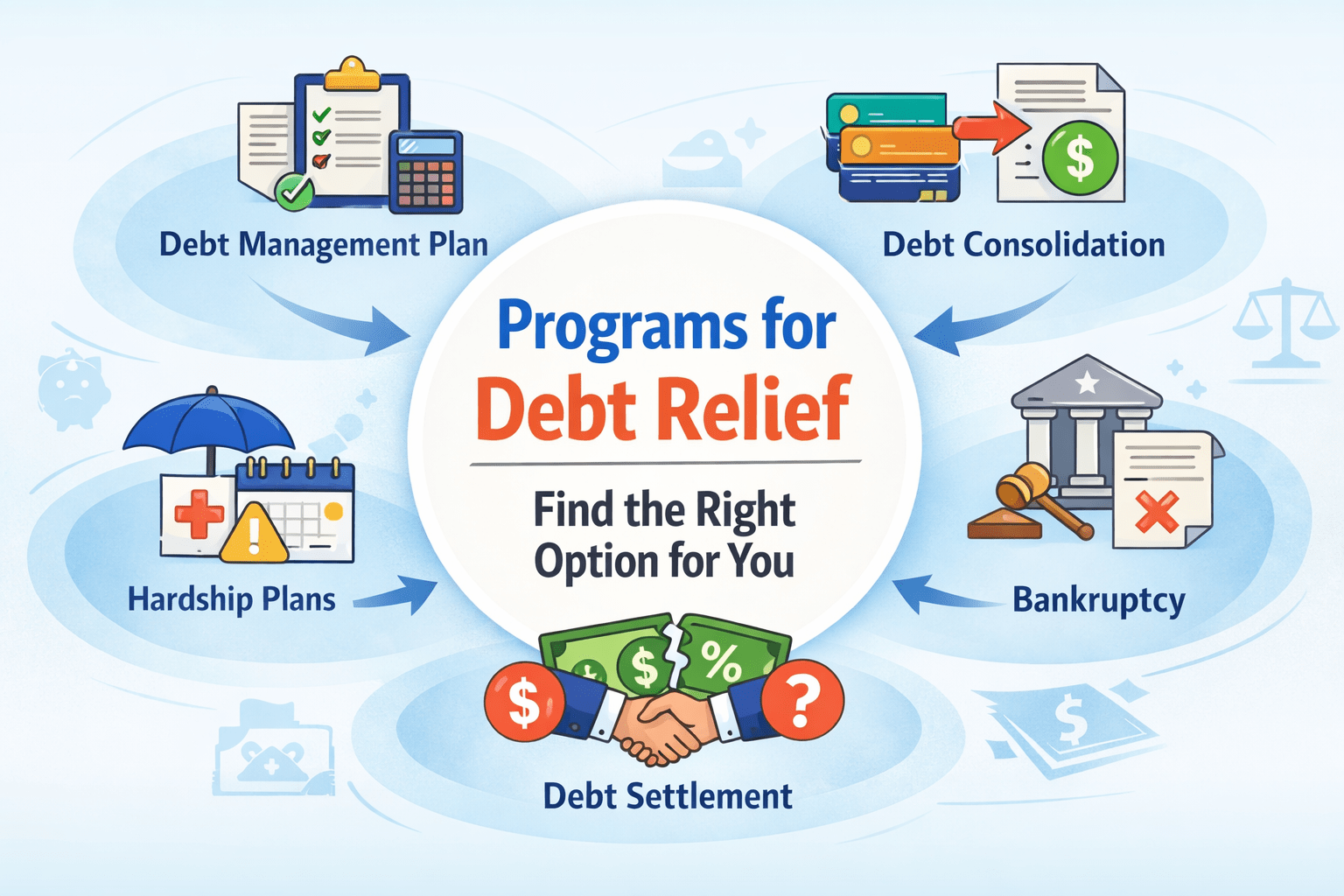

The 5 main types of programs for debt relief

The most common programs for debt relief are:

- Debt management plans

- Debt consolidation

- Hardship plans

- Debt settlement

- Bankruptcy

Each one solves a different kind of problem. Choosing the wrong one can cost you time, money, and peace of mind.

1. Debt management plans

A debt management plan, or DMP, is often a good fit for people who have enough income to repay their unsecured debt, but need lower interest rates and a more manageable monthly payment.

With a DMP, you usually make one monthly payment through a nonprofit credit counseling agency, like Take Charge America. The agency works with your creditors to seek concessions such as reduced interest rates or waived fees. You still repay the debt in full, but the terms may become more realistic.

Best for:

- People with steady income

- Credit card debt and other unsecured debt

- Consumers who are struggling but still have a realistic path to repayment

- People who want help without taking on a new loan

Usually not best for:

- People with no reliable income

- People who are already too far behind to sustain a repayment plan

- Situations where the debt load is far beyond what can reasonably be repaid

For many people comparing programs for debt relief, a DMP is a strong middle-ground option. It offers structure and relief without the severe fallout that can come with settlement or bankruptcy.

2. Debt consolidation

Debt consolidation means replacing multiple debts with one new loan or one new account. This could be a personal loan, a home equity loan, or a balance transfer credit card.

The goal is usually to lower the interest rate, simplify payments, or both.

Best for:

- People with good enough credit to qualify for better terms

- Consumers who are current on payments or only slightly behind

- People who have a clear payoff plan and the discipline to stick to it

Usually not best for:

- People with damaged credit who may not qualify for favorable rates

- Consumers who are already overwhelmed by the payment amount

- Anyone likely to pay off cards and then run them back up again

Debt consolidation can help, but it does not fix the underlying issue by itself. Among programs for debt relief, this option works best when the main problem is high interest, not deeper financial distress.

3. Hardship plans

A hardship plan is temporary relief offered directly by a creditor. It may include a lower payment, reduced interest, paused payments, or another short-term adjustment.

These arrangements are most useful when the problem is temporary, such as a job loss, medical issue, or short-term drop in income.

Best for:

- People facing a temporary setback

- Consumers who expect income to recover soon

- People who are proactive and contact creditors early

Usually not best for:

- Long-term debt problems

- Ongoing overspending issues

- Situations where the monthly payments will still be unaffordable when the hardship period ends

Hardship plans are one of the most overlooked programs for debt relief, but they can be helpful when used early and for the right reason. They are generally a bridge, not a full solution.

4. Debt settlement

Debt settlement usually involves trying to negotiate with creditors so they accept less than the full balance owed. This often happens after accounts have become seriously delinquent.

Some consumers try to settle debts on their own. Others hire a debt settlement company. Either way, this route often comes with major credit damage, collection pressure, and possible tax or legal consequences in some situations.

Best for:

- People with severe unsecured debt problems

- Consumers who are already significantly behind

- People who may be able to offer lump-sum settlements

- Situations where other repayment-based options are no longer realistic

Usually not best for:

- People trying to protect their credit

- Consumers who could still succeed with a DMP or hardship plan

- Anyone expecting an easy or guaranteed outcome

Debt settlement is one of the riskiest programs for debt relief. It can work in some cases, but it is not a clean or painless option.

5. Bankruptcy

Bankruptcy is a legal process that may eliminate certain debts or create a court-supervised repayment structure, depending on the type filed. It is usually the most serious debt relief option and should be discussed with a qualified bankruptcy attorney.

Best for:

- People with no realistic path to repay what they owe

- Consumers facing lawsuits, wage garnishment, or severe financial distress

- Situations where other options are no longer workable

Usually not best for:

- People who can still reasonably resolve their debt through counseling, repayment, or temporary relief

- Consumers making a decision without legal advice

Among all programs for debt relief, bankruptcy has the most serious long-term consequences, particularly when it comes to your credit, but it can also provide needed protection and a real fresh start for people in deep financial trouble.

How to choose the right debt relief option

If you are comparing programs for debt relief, ask yourself these questions:

Is your problem temporary or ongoing?

If your income should recover soon, a hardship plan may be enough. If the problem has been building for a long time, you may need a more structured solution.

Can you repay the debt with lower payments or lower interest?

If yes, a debt management plan (DMP) may be worth exploring. If no, then settlement or bankruptcy may need to be part of the conversation.

Is your credit still strong?

If you still have good credit and can qualify for a lower-rate loan, debt consolidation may help. If your credit is already damaged, that option may not be available or helpful.

Are you already seriously behind?

If you are severely delinquent, some options may no longer be realistic. At that stage, settlement or bankruptcy may be more relevant than consolidation.

Do you want to avoid taking on new debt?

A debt management plan (DMP) may appeal to people who want to address existing debt without replacing it with a new loan.

Which debt relief option should you start with?

Because the best option can change quickly based on income, delinquency, and the type of debt you have, it usually makes sense to start with a professional review of your situation.

A nonprofit credit counselor can help you compare programs for debt relief, understand the tradeoffs, and identify whether a debt management plan, hardship strategy, consolidation, settlement, or bankruptcy referral makes the most sense.

If you are struggling with unsecured debt and are not sure where to begin, speaking with a certified credit counselor can help you make a more informed decision before the problem gets worse.

Take Charge America may be able to help you with a DMP. Call 877-357-6309 to speak with a counselor, or click here to get a free, personalized online quote in minutes with no impact to your credit score.

FAQ

What are the main programs for debt relief?

The five main programs for debt relief are debt management plans, debt consolidation, hardship plans, debt settlement, and bankruptcy.

Which debt relief option is best for credit card debt?

It depends on the situation. For someone with steady income who can repay the debt with lower interest rates, a debt management plan may be a good fit. For someone with strong credit, consolidation may help. For severe financial distress, settlement or bankruptcy may be more appropriate.

Is debt settlement the same as a debt management plan?

No. A debt management plan is designed to help you repay your debt in full under more manageable terms. Debt settlement involves trying to pay less than the full balance and usually comes with more serious consequences.

Are hardship plans a long-term solution?

Usually not. Hardship plans are generally temporary arrangements intended to help during short-term financial setbacks.

When should someone consider bankruptcy?

Bankruptcy may be worth discussing with an attorney when there is no realistic path to repay the debt and other options are no longer workable.

Related Posts

Preparing for a Recession: Save Money or Pay Off Debt?

Many economists agree that the United States is like to enter a recession sometime soon. This can be unsettling, especially…

Read More

Do’s and Don’ts of Negotiating Credit Card Interest Rates

Credit card interest rates aren’t etched in stone. In order to retain business creditors may lower the interest rates of…

Read More

What You Need to Know about Deposit Insurance in the U.S.

Exactly Who Insures What for Whom? Types of insurance plans in use today: 1. The U.S. Government accumulates a fund…

Read More